Authored by Tom Luongo via Gold, Goats, 'n Guns blog,

A few months ago I talked about the upcoming changes to the way adoption of Basel III?s new bank reserve rules would alter the gold market.

In short my conclusion was similar to that of Alistair MacLeod?s and others, that Basel III should collapse the egregious manipulation of the gold market through the use of using futures and unallocated gold as bank reserves.

In May I wrote:

In effect, Basel III, if implemented in its current form, would change the gold market from a speculative one based on perceptions of the efficacy of monetary policy to control real interest rates to one that should force price discovery in an almost purely physical market. As I told my Patrons in May 16th?s Market Report video, physical gold will go from being the price taker to the price maker.

I didn?t then nor do I think now that will happen immediately after Basel III goes into effect in the U.K. on January 1st. But I do think the recent weakness in gold has been an early sign of stress within the gold market brought on by the upcoming rules implementations.

And that has sent gold lower in recent weeks despite rising inflation and falling real interest rates. Of course this is because the markets have been overpricing the ?transitory inflation? argument put forth by the major central banks.

So, when Jerome Powell came out, in his first important statement post-reappointment announcement, and put a fork in ?transitory? inflation the markets were properly shocked. This happened on the heels of OmicronVID-9/11 dominating the headlines and also creating some overblown market reactions thanks to poorly-programmed headline trading algorithms.

For those who have been confused or disagreed with my assessment of Powell for the past six months, thinking Powell was lying about inflation as proof he?s just another idiot Fed Chair, I give you the counter argument. He had to survive the obvious coup attempt put on by Obama and Lael Brainard to oust those not controlled by Davos from the FOMC.

Once that happened, Powell could speak openly because the political storm clouds over his head dissipated. Cue his forcing Treasury Secretary Janet Yellen to finally agree with him on inflation after he put his cards on the table.

Now, we have policy clarity from the Fed.

They will be tapering QE and they will be raising rates in 2022. Now the markets can begin the task of readjusting themselves into year-end. With that in mind, it makes perfect sense to see gold, which has been a losing trade all year under pressure just from tax-loss selling alone, no less expectations of a stronger U.S. dollar.

It also makes sense for high-flying equities to take a hit along with junk bonds which were yielding less than inflation. There are trillions in misallocated capital out there that go far beyond the simple idea that the Fed?s only mandate is to prop up the equity markets.

Powell and those that stand behind him, I have strenuously argued, can see the fight for the future of the monetary system clearly, and it doesn?t include a place for the commercial banks in a world of CBDCs. While one could argue the Fed would like that power CBDCs confer, one could also clearly make the counter argument that it also loses a tremendous amount of power now being just one central bank among many and the dollar just another digital token without value.

Does anyone really believe Wall St. is happy to sign up for this nonsense? City of London?

To get a really good sense of where I think we are in this now, check out my recent appearance on Bitcoin Magazine?s Fed Watch Podcast and Livestream.

Okay so, all that said, let?s really talk about what?s happening in gold.

Because this week we saw two major announcements by two very different central banks vis a vis gold.

All Roads to Singapore

Singapore has now joined the ranks of Russia, Turkey, Hungary, Serbia, Poland and others in adding to their central bank gold reserves. This is a very significant move because this is the first country outside of those in Russia?s nominal orbit.

Singapore, outside of Hong Kong, is a major clearinghouse for offshore Chinese yuan settlements. ICBC opened up a branch there in 2012 to handle such transactions and things have only progressed from there.

I don?t necessarily see this as a China-related move by the MAS ? Monetary Authority of Singapore ? as their monetary policy is very independent and pretty much algorithmic.

They manage the exchange rate of the Singapore dollar (SGD) within a 1% band of expected rates against a basket of currencies, rather than publishing a benchmark rate. Moreover, the MAS is moving away from the old SIBOR / SOR system. SIBOR is Singaporean LIBOR ? the interbank overnight lending rate. And SOR is the SGD overnight swap rate.

They, like the U.S., are move to an analogue of SOFR ? the Secured Overnight Funding Rate ? to replace LIBOR. SORA is Singaporean SOFR for all intents and purposes.

So, why is this important?

If Singapore is worried, like everyone else is about a collapse of the current financial system which is expressly on the table via Davos and the Great Reset, then those with the gold will be in a much better position to defend their currencies during a crisis and maintain a relatively stable global exchange rate.

Since Singapore aims to be the independent broker between East and West, especially now that Hong Kong has all but been taken over by China, this move is very interesting to say the least.

From the Zerohedge article on this there?s is this great point:

For a central bank which actively publishes reams of publications and reports on all sorts of topics related to Singapore?s financial sector and markets and it?s international financial position, this omission about Singapore?s sizeable gold purchases could be considered quite strange, but then again, given that we are dealing with the secretive world of gold and central banks, maybe it?s not so strange.

In addition, MAS is famous for it?s obsession with maintaining and controlling the exchange rate of the Singaporean dollar (versus a basket of currencies), so perhaps MAS prefers not to draw attention to the amount of gold in it?s international reserves as this might encourage FX markets to view the gold purchase as a move that strengthens Singapore?s reserve position and hence could put upward pressure on it?s exchange rate.

Singapore is a key player for the future of pan-Asian finance. If the very savvy MAS is buying gold then they are scared. They are making plans for a very different future where debt becomes the dirtiest word in English.

Moreover, they bought this gold back in May and June and it has only now been discovered on their balance sheet. Why would they not announce these purchases?

For the same reason the Bank of Ireland didn?t tell anyone they nibbled on some physical gold over the summer, so as to not move the price. What?s really significant here is that Ireland is the first euro-zone country to announce gold purchases. Previous to this it was only non-euro EU members like Hungary, Poland and Czechia.

That we?re seeing euro-zone countries begin shoring up their currency reserves with gold feeds the argument I made back in May.

Moreover, just so everyone is also clear what both of these central banks are facing, it isn?t just Europe that is now dealing with insane natural gas prices. Singapore is looking at a catastrophic rise in energy costs. So, if you think the MAS isn?t still toe-dipping without telling anyone into gold to stabilize the SingDollar well, you have a reading comprehension problem.

The Golden Circle

Now let?s go back to Basel III and talk about how it was supposed to be the thing that finally got gold out of its slump.

Back in May, Powell hadn?t begun defending the U.S. dollar. He hadn?t even had his public spat with ECB President Christine Lagarde yet. Nor had he raised the Reverse Repo Rate he was paying to 0.05%.

So, with Basel III on the horizon and the U.K. exempt until January 1st, 2022, there is still the basic infrastructure in place that if the Fed tightens, which it did through the RRP rate, then gold would be under constant pressure by those needing dollars at cheap rates regardless of the fundamentals.

Short term funding needs always trump long-term fundamentals.

So, the Fed still needs gold kept under wraps to maintain its primacy. But at the same time, the ECB and other Central Banks accumulating gold need it to rise, or at least keep pace with their currency vs. the dollar.

I still believe that dynamic is in play for 2022 and it will finally be the full expression of Basel III that will continue putting a higher floor underneath gold.

Remember, as I wrote back in that May article:

The ECB, on the other hand [vs. the Fed], can go bankrupt, since it has no capacity to [create infinite amounts of elastic money]. All it can do is buy the sovereign debt of the member countries? central banks and hand them back euros, while swapping around deckchairs on this monetary Titanic. There is a definable limit to this process, especially if rates rise as people lose confidence in the underlying economic activity of those countries and their fiscal positions.

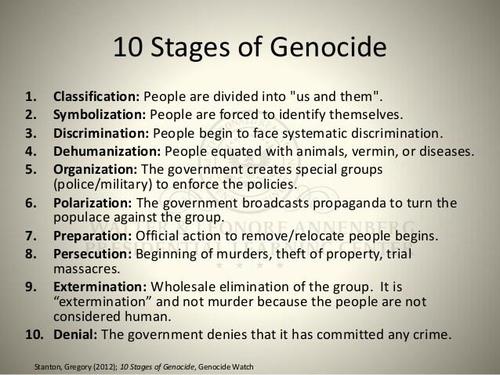

Europe is locking down its economy over OmicronVID-9/11 and removing the unvaccinated from society. They are between steps 7 and 8of 10 on the path to genocide.

Does any rational person believe there will be a renaissance of European economic dynamism in 2022 under these conditions? If you do, you might be a shitlib who believes in unicorn farts, 69 genders and that Elizabeth Warren is an economic genius.

For the rest of us who live in reality-land, of course Europe is the most vulnerable here.

Once Basel III goes fully into effect and paper and unallocated physical gold will no longer be considered as bank collateral for balance sheet purposes, the demand for physical gold because of this need for it as a central bank asset to back national currencies, becomes even more acute.

Those countries lining up on the opposite side of the Great Reset are buying gold while it is still cheap. Powell?s dollar drain since June?s RRP rate hike has gifted everyone with cheaper gold prices for another 6 months.

The MAS buying gold is telling you that what I said back in May is reality:

So, Basel III is coming to destroy the paper gold markets and destroy the money center banks in New York and London while setting the stage to bail out the euro-zone. Higher gold prices are the answer to all of these things. Think of it this way, in a world where debt assets are failing and new private forms of custodial assets are rising in mindshare [bitcoin and crypto], what?s the only real weapon the central banks have to maintain credibility?

Their gold reserves.

This is the essence of why Davos, I think inadvertently, is creating the new role for gold during these times of change.

For the ECB to survive the bankruptcy of Europe gold has to rise.

For emerging market central banks to survive the turmoil unleashed by an epic U.S. dollar rally because of Europe?s bankruptcy gold has to rise.

When China decides to assert itself as the dominant economic player, which I think it would do in the event of a kinetic conflict between it and the U.S., it?s first move will be upwardly revising its official gold reserves? by a lot.

Gold will really rise on that.

The Great Quagmire

Remember the entire Great Reset rests on Davos destroying the current banking system and rolling it up to the central banks, cutting out the classic two-track monetary system with the commercial bankers being the transmission mechanism.

It means them getting control over the Fed, which looks like a lost cause now. Powell is fully in control of FOMC policy, which I expect him to make very clear at the next meeting. This is why Pelosi so easily cut a deal over the debt ceiling.

There will be no further stupid and dangerous brinksmanship calling into question U.S. policy. The markets are demanding clarity from the U.S. Davos? manufactured chaos through the Democrats? shenanigans on Capitol Hill should be a thing of the past. That alone will help push capital back towards the U.S.

Davos? agenda has failed on Capitol Hill, despite winning battles all across Europe and in the English Commonwealth. Those countries are now dead letters until their current governments are overthrown or the people throw off their shackles? not likely.

Despite the market jitters because of the necessary reallocation to global capital, Powell and the Fed now have to pursue tight monetary policy to force the ECB into openly inflationary policy. This will further trash the euro and finally overwhelm the ECB?s bond buying to the point where rates there start rising.

Davos has responded with gutting Europe to the bone with OmicronVID-9/11 lockdowns and forced vaccinations to take down the global demand side of the monetary equation while forcing diplomatic conflicts on China and Russia neither want to stop the flow of goods around the world.

This is why NATO and the Neocons are going wild in Eastern Europe.

It?s why the Israelis are threatening a war with Iran.

And it?s why the O?Biden administration is looking increasingly desperate to bring us to the brink of war without there actually being one.

Just enough conflict, sanctions, sabre rattling and embarrassments to upset China and Russia?s domestic politics while draining them of their economic dynamism through provocations in places like Afghanistan, Syria, Ukraine, Belarus and yes, even Taiwan while trying to force energy prices higher.

Europe is Davos? power base. That power looks tenuous at best in a geopolitical sense. The best way for it to reassert what power it has left over the U.S. is forcing a massive revaluation in the price of gold while preparing Europe for further federalization, debt default and population reduction, as I discussed in my last article.

The main path for the central banks to maintain any semblance of credibility in the minds of investors rightly freaked out over the events of the past two years is to add to their gold reserves to offset any currency risk to their fiat reserves.

And while the Fed has fought the good fight against this, with the end of QE and rising rates, a flattening yield curve and more turmoil in overseas funding markets as a result of a much stronger dollar, gold will assert itself (alongside bitcoin) as the safe haven asset of choice in 2022.

So, watch the news flow for more signs of Central Bank gold purchases.

So far in 2021, through September, according to the World Gold Council, central banks have purchased 385.4 tonnes of gold, after adding Singapore?s numbers but not Ireland?s. This is roughly on track with expectations for this year of around 15% of total gold demand.

If not for Turkey?s net outflows thanks to the collapse of its banking system (-27.8 tonnes) and the Philippines who sell local mine production to finance the government, the demand would be well over 400 tonnes this year.

But, as I said throughout this piece, it is the players who are doing this now that matters. Earlier Japan made headlines, adding 80.8 tonnes in March. Then Poland began a very Russian monthly buying program in May. Now Singapore is on board trying to offset US dollar strength with gold in an inflationary environment.

And the Irish are now trying to stave off a monetary famine in Europe.

The times they are a?changing rapidly.

A few months ago I talked about the upcoming changes to the way adoption of Basel III?s new bank reserve rules would alter the gold market.

In short my conclusion was similar to that of Alistair MacLeod?s and others, that Basel III should collapse the egregious manipulation of the gold market through the use of using futures and unallocated gold as bank reserves.

In May I wrote:

In effect, Basel III, if implemented in its current form, would change the gold market from a speculative one based on perceptions of the efficacy of monetary policy to control real interest rates to one that should force price discovery in an almost purely physical market. As I told my Patrons in May 16th?s Market Report video, physical gold will go from being the price taker to the price maker.

I didn?t then nor do I think now that will happen immediately after Basel III goes into effect in the U.K. on January 1st. But I do think the recent weakness in gold has been an early sign of stress within the gold market brought on by the upcoming rules implementations.

And that has sent gold lower in recent weeks despite rising inflation and falling real interest rates. Of course this is because the markets have been overpricing the ?transitory inflation? argument put forth by the major central banks.

So, when Jerome Powell came out, in his first important statement post-reappointment announcement, and put a fork in ?transitory? inflation the markets were properly shocked. This happened on the heels of OmicronVID-9/11 dominating the headlines and also creating some overblown market reactions thanks to poorly-programmed headline trading algorithms.

For those who have been confused or disagreed with my assessment of Powell for the past six months, thinking Powell was lying about inflation as proof he?s just another idiot Fed Chair, I give you the counter argument. He had to survive the obvious coup attempt put on by Obama and Lael Brainard to oust those not controlled by Davos from the FOMC.

Once that happened, Powell could speak openly because the political storm clouds over his head dissipated. Cue his forcing Treasury Secretary Janet Yellen to finally agree with him on inflation after he put his cards on the table.

Now, we have policy clarity from the Fed.

They will be tapering QE and they will be raising rates in 2022. Now the markets can begin the task of readjusting themselves into year-end. With that in mind, it makes perfect sense to see gold, which has been a losing trade all year under pressure just from tax-loss selling alone, no less expectations of a stronger U.S. dollar.

It also makes sense for high-flying equities to take a hit along with junk bonds which were yielding less than inflation. There are trillions in misallocated capital out there that go far beyond the simple idea that the Fed?s only mandate is to prop up the equity markets.

Powell and those that stand behind him, I have strenuously argued, can see the fight for the future of the monetary system clearly, and it doesn?t include a place for the commercial banks in a world of CBDCs. While one could argue the Fed would like that power CBDCs confer, one could also clearly make the counter argument that it also loses a tremendous amount of power now being just one central bank among many and the dollar just another digital token without value.

Does anyone really believe Wall St. is happy to sign up for this nonsense? City of London?

To get a really good sense of where I think we are in this now, check out my recent appearance on Bitcoin Magazine?s Fed Watch Podcast and Livestream.

Okay so, all that said, let?s really talk about what?s happening in gold.

Because this week we saw two major announcements by two very different central banks vis a vis gold.

All Roads to Singapore

Singapore has now joined the ranks of Russia, Turkey, Hungary, Serbia, Poland and others in adding to their central bank gold reserves. This is a very significant move because this is the first country outside of those in Russia?s nominal orbit.

Singapore, outside of Hong Kong, is a major clearinghouse for offshore Chinese yuan settlements. ICBC opened up a branch there in 2012 to handle such transactions and things have only progressed from there.

I don?t necessarily see this as a China-related move by the MAS ? Monetary Authority of Singapore ? as their monetary policy is very independent and pretty much algorithmic.

They manage the exchange rate of the Singapore dollar (SGD) within a 1% band of expected rates against a basket of currencies, rather than publishing a benchmark rate. Moreover, the MAS is moving away from the old SIBOR / SOR system. SIBOR is Singaporean LIBOR ? the interbank overnight lending rate. And SOR is the SGD overnight swap rate.

They, like the U.S., are move to an analogue of SOFR ? the Secured Overnight Funding Rate ? to replace LIBOR. SORA is Singaporean SOFR for all intents and purposes.

So, why is this important?

If Singapore is worried, like everyone else is about a collapse of the current financial system which is expressly on the table via Davos and the Great Reset, then those with the gold will be in a much better position to defend their currencies during a crisis and maintain a relatively stable global exchange rate.

Since Singapore aims to be the independent broker between East and West, especially now that Hong Kong has all but been taken over by China, this move is very interesting to say the least.

From the Zerohedge article on this there?s is this great point:

For a central bank which actively publishes reams of publications and reports on all sorts of topics related to Singapore?s financial sector and markets and it?s international financial position, this omission about Singapore?s sizeable gold purchases could be considered quite strange, but then again, given that we are dealing with the secretive world of gold and central banks, maybe it?s not so strange.

In addition, MAS is famous for it?s obsession with maintaining and controlling the exchange rate of the Singaporean dollar (versus a basket of currencies), so perhaps MAS prefers not to draw attention to the amount of gold in it?s international reserves as this might encourage FX markets to view the gold purchase as a move that strengthens Singapore?s reserve position and hence could put upward pressure on it?s exchange rate.

Singapore is a key player for the future of pan-Asian finance. If the very savvy MAS is buying gold then they are scared. They are making plans for a very different future where debt becomes the dirtiest word in English.

Moreover, they bought this gold back in May and June and it has only now been discovered on their balance sheet. Why would they not announce these purchases?

For the same reason the Bank of Ireland didn?t tell anyone they nibbled on some physical gold over the summer, so as to not move the price. What?s really significant here is that Ireland is the first euro-zone country to announce gold purchases. Previous to this it was only non-euro EU members like Hungary, Poland and Czechia.

That we?re seeing euro-zone countries begin shoring up their currency reserves with gold feeds the argument I made back in May.

Moreover, just so everyone is also clear what both of these central banks are facing, it isn?t just Europe that is now dealing with insane natural gas prices. Singapore is looking at a catastrophic rise in energy costs. So, if you think the MAS isn?t still toe-dipping without telling anyone into gold to stabilize the SingDollar well, you have a reading comprehension problem.

The Golden Circle

Now let?s go back to Basel III and talk about how it was supposed to be the thing that finally got gold out of its slump.

Back in May, Powell hadn?t begun defending the U.S. dollar. He hadn?t even had his public spat with ECB President Christine Lagarde yet. Nor had he raised the Reverse Repo Rate he was paying to 0.05%.

So, with Basel III on the horizon and the U.K. exempt until January 1st, 2022, there is still the basic infrastructure in place that if the Fed tightens, which it did through the RRP rate, then gold would be under constant pressure by those needing dollars at cheap rates regardless of the fundamentals.

Short term funding needs always trump long-term fundamentals.

So, the Fed still needs gold kept under wraps to maintain its primacy. But at the same time, the ECB and other Central Banks accumulating gold need it to rise, or at least keep pace with their currency vs. the dollar.

I still believe that dynamic is in play for 2022 and it will finally be the full expression of Basel III that will continue putting a higher floor underneath gold.

Remember, as I wrote back in that May article:

The ECB, on the other hand [vs. the Fed], can go bankrupt, since it has no capacity to [create infinite amounts of elastic money]. All it can do is buy the sovereign debt of the member countries? central banks and hand them back euros, while swapping around deckchairs on this monetary Titanic. There is a definable limit to this process, especially if rates rise as people lose confidence in the underlying economic activity of those countries and their fiscal positions.

Europe is locking down its economy over OmicronVID-9/11 and removing the unvaccinated from society. They are between steps 7 and 8of 10 on the path to genocide.

Does any rational person believe there will be a renaissance of European economic dynamism in 2022 under these conditions? If you do, you might be a shitlib who believes in unicorn farts, 69 genders and that Elizabeth Warren is an economic genius.

For the rest of us who live in reality-land, of course Europe is the most vulnerable here.

Once Basel III goes fully into effect and paper and unallocated physical gold will no longer be considered as bank collateral for balance sheet purposes, the demand for physical gold because of this need for it as a central bank asset to back national currencies, becomes even more acute.

Those countries lining up on the opposite side of the Great Reset are buying gold while it is still cheap. Powell?s dollar drain since June?s RRP rate hike has gifted everyone with cheaper gold prices for another 6 months.

The MAS buying gold is telling you that what I said back in May is reality:

So, Basel III is coming to destroy the paper gold markets and destroy the money center banks in New York and London while setting the stage to bail out the euro-zone. Higher gold prices are the answer to all of these things. Think of it this way, in a world where debt assets are failing and new private forms of custodial assets are rising in mindshare [bitcoin and crypto], what?s the only real weapon the central banks have to maintain credibility?

Their gold reserves.

This is the essence of why Davos, I think inadvertently, is creating the new role for gold during these times of change.

For the ECB to survive the bankruptcy of Europe gold has to rise.

For emerging market central banks to survive the turmoil unleashed by an epic U.S. dollar rally because of Europe?s bankruptcy gold has to rise.

When China decides to assert itself as the dominant economic player, which I think it would do in the event of a kinetic conflict between it and the U.S., it?s first move will be upwardly revising its official gold reserves? by a lot.

Gold will really rise on that.

The Great Quagmire

Remember the entire Great Reset rests on Davos destroying the current banking system and rolling it up to the central banks, cutting out the classic two-track monetary system with the commercial bankers being the transmission mechanism.

It means them getting control over the Fed, which looks like a lost cause now. Powell is fully in control of FOMC policy, which I expect him to make very clear at the next meeting. This is why Pelosi so easily cut a deal over the debt ceiling.

There will be no further stupid and dangerous brinksmanship calling into question U.S. policy. The markets are demanding clarity from the U.S. Davos? manufactured chaos through the Democrats? shenanigans on Capitol Hill should be a thing of the past. That alone will help push capital back towards the U.S.

Davos? agenda has failed on Capitol Hill, despite winning battles all across Europe and in the English Commonwealth. Those countries are now dead letters until their current governments are overthrown or the people throw off their shackles? not likely.

Despite the market jitters because of the necessary reallocation to global capital, Powell and the Fed now have to pursue tight monetary policy to force the ECB into openly inflationary policy. This will further trash the euro and finally overwhelm the ECB?s bond buying to the point where rates there start rising.

Davos has responded with gutting Europe to the bone with OmicronVID-9/11 lockdowns and forced vaccinations to take down the global demand side of the monetary equation while forcing diplomatic conflicts on China and Russia neither want to stop the flow of goods around the world.

This is why NATO and the Neocons are going wild in Eastern Europe.

It?s why the Israelis are threatening a war with Iran.

And it?s why the O?Biden administration is looking increasingly desperate to bring us to the brink of war without there actually being one.

Just enough conflict, sanctions, sabre rattling and embarrassments to upset China and Russia?s domestic politics while draining them of their economic dynamism through provocations in places like Afghanistan, Syria, Ukraine, Belarus and yes, even Taiwan while trying to force energy prices higher.

Europe is Davos? power base. That power looks tenuous at best in a geopolitical sense. The best way for it to reassert what power it has left over the U.S. is forcing a massive revaluation in the price of gold while preparing Europe for further federalization, debt default and population reduction, as I discussed in my last article.

The main path for the central banks to maintain any semblance of credibility in the minds of investors rightly freaked out over the events of the past two years is to add to their gold reserves to offset any currency risk to their fiat reserves.

And while the Fed has fought the good fight against this, with the end of QE and rising rates, a flattening yield curve and more turmoil in overseas funding markets as a result of a much stronger dollar, gold will assert itself (alongside bitcoin) as the safe haven asset of choice in 2022.

So, watch the news flow for more signs of Central Bank gold purchases.

So far in 2021, through September, according to the World Gold Council, central banks have purchased 385.4 tonnes of gold, after adding Singapore?s numbers but not Ireland?s. This is roughly on track with expectations for this year of around 15% of total gold demand.

If not for Turkey?s net outflows thanks to the collapse of its banking system (-27.8 tonnes) and the Philippines who sell local mine production to finance the government, the demand would be well over 400 tonnes this year.

But, as I said throughout this piece, it is the players who are doing this now that matters. Earlier Japan made headlines, adding 80.8 tonnes in March. Then Poland began a very Russian monthly buying program in May. Now Singapore is on board trying to offset US dollar strength with gold in an inflationary environment.

And the Irish are now trying to stave off a monetary famine in Europe.

The times they are a?changing rapidly.